Why High-Net-Worth Individuals May Not Be Able to Afford to Overlook This Key Protection

Even the most financially savvy people can have blind spots in their financial strategy. One area frequently overlooked, even by those who have diligently built substantial wealth, is disability protection insurance.

For high-net-worth individuals approaching retirement, disability protection isn't just another insurance product—it's a potentially critical component of preserving the wealth you've worked decades to accumulate.

Even high-earning professionals can face significant financial strain if their income is interrupted. To help prevent that and protect your retirement, let's examine five key misconceptions about disability protection that could put your retirement plans at risk.

Misconception #1: "Social Security will cover my needs if I become disabled"

Many successful professionals and executives assume government programs provide adequate disability protection. The reality tells a different story: the average monthly Social Security Disability Insurance (SSDI) benefit is approximately $1,580, far below what many high-net-worth individuals need to maintain their lifestyle.

What's more concerning is how much these benefits are being depleted. The Social Security Disability Insurance program paid out over $150 billion in benefits in 2023, and the system is expected to exhaust its reserves by the end of 2035 if changes aren't made. For those nearing retirement with sophisticated financial needs, relying solely on government benefits can create substantial risk to your long-term financial security.

Misconception #2: "Disability primarily happens due to accidents, which won't affect me"

Oftentimes when people hear "disability," they immediately think of accidents or injuries. However, the data reveals a surprising truth:

· Musculoskeletal/connective tissue disorders account for 24% of disability claims

· Mental disorders represent 14% of claims

· Accidents/injuries make up just 11% of disability cases

· Other leading causes include nervous system disorders (9%), circulatory conditions (9%), and cancer (8%)

These statistics, based on MassMutual claims data from 1972-2022, show that nearly 90% of disabilities are caused by illnesses rather than accidents. For high-net-worth individuals approaching retirement, these health-related risks increase with age, precisely when you can least afford a disruption to your income or retirement savings strategy.

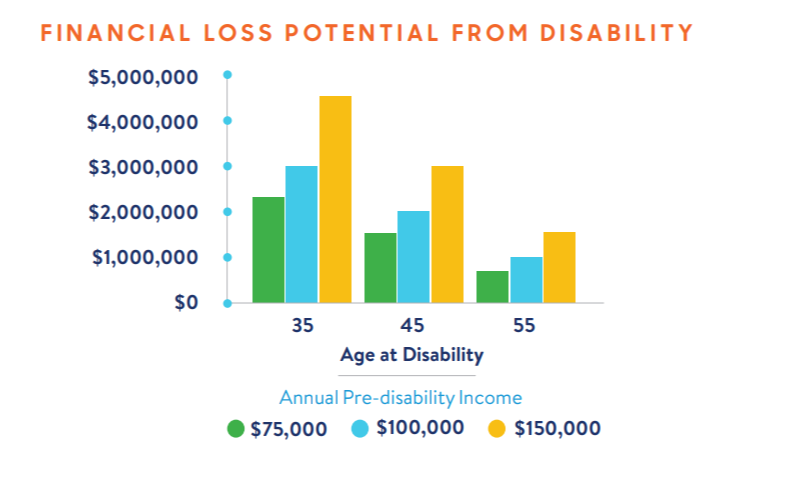

Misconception #3: "I don't need disability protection as I approach retirement"

Many clients tell us, "I'm only a few years from retirement, so disability insurance isn't relevant for me." This perspective overlooks a critical reality: the years immediately preceding retirement are often your peak earning period when a disability could have the most devastating financial impact.

Consider the chart of financial loss projections from MassMutual: a 55-year-old executive earning $150,000 annually could lose $1.5 million in income if disabled until retirement age. That doesn't account for the lost retirement contributions, potential early withdrawal of retirement assets, and additional medical expenses that often accompany a disability.

These pre-retirement years are when your financial strategy can be most vulnerable to disruption—and when comprehensive protection is most vital.

Misconception #4: "My employer's disability coverage is sufficient protection"

Many executives and professionals have some disability coverage through their employers. However, there are several limitations to employer-provided coverage that high-net-worth individuals should understand:

· Most group policies replace only 50-60% of your base salary

· Many policies cap monthly benefits at levels insufficient for high earners

· Bonuses, commissions, and other incentive compensation are typically excluded

· Benefits are usually taxable when premiums are employer-paid

· Coverage terminates when you leave the company

For high-income professionals and business owners, employer coverage often creates a false sense of security while leaving potentially significant income gaps unprotected.

Misconception #5: "Disability insurance is a standalone product rather than part of a comprehensive plan"

Perhaps the most dangerous misconception is viewing disability protection in isolation rather than as an integrated component of your wealth management strategy.

Disability protection influences numerous aspects of your financial strategy:

· Income protection during your highest earning years

· Preservation of retirement savings

· Business continuation planning for entrepreneurs

· Tax-efficient wealth transfer strategies

· Integration with long-term care planning

Without proper coordination, gaps in your protection strategy can undermine decades of careful financial planning.

Taking Action: Review Your Disability Protection Strategy

As part of a comprehensive financial review, it's essential to evaluate your disability protection strategy regularly. Consider these important questions:

· How would a disability affect your retirement timeline and income needs?

· Does your current coverage adequately protect your specific income sources?

· How does your disability protection integrate with your tax and estate planning?

· If you're a business owner, how would your company and personal finances withstand your disability?

Partner with OneTeam Who Understands Your Complete Financial Picture

At OneTeam Financial, we specialize in helping high-net-worth individuals approaching retirement develop integrated financial strategies that protect what they've built while optimizing for the future.

Our subject matter specialists work collaboratively to help ensure every aspect of your financial life is working in harmony—including appropriate disability protection that safeguards your retirement plans and preserves the legacy you've worked so hard to build.

Don't let misconceptions about disability protection put your financial future at risk. Contact our team todayto schedule a comprehensive review of your protection strategy as part of your overall financial plan.